By Tom Woods

On October 31st, 2008, an unknown individual or group working under the mysterious pseudonym “Satoshi Nakamoto” sent an email with a link to a white paper titled “Bitcoin: A Peer-to-Peer Electronic Cash System” to a cryptographic mailing list. It outlined a revolutionary plan to create a digital currency which would rely not on intermediaries or people’s trust in central banks, but a new technology called blockchain. Bitcoin officially launched two months later and almost immediately drew attention from cryptographers and some fringe investors. Hype around the technology swirled then suddenly built to a crescendo in 2017, when the price of a single bitcoin boomed from $900 to $20,000 in the space of 12 months. By this point, IBM had launched its own blockchain ecosystem, while publications such as the Wall Street Journal were touting it as a world-changer. The rise of cryptocurrencies and integration of blockchain into every industry imaginable seemed inevitable, but, just a few months later, the hype had crashed.

First, bitcoin’s “bubble” burst, with its price plummeting down to $7,000 by February 2018, then $3,500 by November 2018. This was followed by severely negative press and an emerging consensus that blockchain had practically no potential to change the world. Critics argued that it was a damp squib, an overhyped and unoriginal technology that in over ten years had achieved little other than facilitate illegal transactions and make the fortunes of a handful of shrewd investors. Nowadays, other than the occasional bizarre Elon Musk tweet or usage in scams, news about blockchain rarely penetrates the mainstream. Despite this, the technology retains a hardcore of believers who remain committed to the idea of it as the postmodern epoch’s answer to the printing press. Though exaggerated, this view comes a lot closer to the truth than that which most commentators pedal nowadays. Blockchain isn’t going to bring about a sudden revolution that overhauls how the world functions, but, used in conjunction with other technologies, will lead to subtle yet powerful changes to industry and government. Indeed, much of this change is already in progress, and while the media and public turn a blind eye, industry leaders are ramping up investments.

One of the chief barriers to widespread enthusiasm about blockchain is its complex and sometimes dreary nature. Indeed, unlike innovations such as the internet, it can be difficult for the non-specialist to gain a basic understanding of it, let alone want to gain a basic understanding of it. It’s therefore worth providing a brief explanation of what the technology is and the problems it seeks to address.

At its core, a blockchain is a database. What makes it unique is that instead of being stored on one centralised device/computer (also known as a node), it is distributed in an encrypted form amongst multiple nodes. Furthermore, each piece of data on the blockchain is verified by people using nodes with massive computing power (otherwise known as miners). Data is then lumped into blocks, which are then linked to other blocks, meaning that hacking into a blockchain and changing data already on it entails changing multiple encrypted blocks on multiple nodes. Though not impossible, the cost of such a hack is largely deemed counterproductive, as the computing power needed to undertake it would usually be greater than any potential gain. In theory, blockchain is thus able to create immutable databases that are better at storing data than conventional ones.

Though it might sound exceptionally unglamorous at a first glance, if this feature of blockchain works properly, it has the potential to achieve two very important things: remove unnecessary intermediaries from the process of transactions and allow for better record-keeping. Today, consumers (often unknowingly) place massive amounts of trust in institutions such as central banks and energy companies to smoothly carry out the most important transactions to their lives. For instance, something as menial as scanning a card to pay for groceries can involve multiple institutions working to approve the action and then taking a cut. With people’s faith in these intermediaries waning following issues such as security breaches and concerns over malicious agendas, blockchain can step in and offer the consumer a genuine alternative to the current model. Through it, consumers can reposition their trust that a transaction will be properly carried out from intermediaries to the system of miners who verify all data on blockchains. In theory, this could lead to quicker transactions as well as transactions between actors who do not know or trust one another. Its potential to create better record-keeping systems could be even greater. Here, blockchain could help to curb government corruption by providing people with better proof of ownership of assets such as property or give consumers better information about products in the form of immutable descriptions of their properties, to name just two examples. So, what progress has blockchain made in realising its potential? And what barriers to success stand in its way?

As a fairly nascent technology, blockchain’s progress in penetrating various industries remains asymmetric. Best known for its influence in finance, this is probably where the technology has had and will have the greatest impact. Already, numerous firms have implemented blockchain databases to help their processes of reconciliation. This is an accounting process whereby two or more data sets across different departments or firms are reviewed to check that there are no inconsistencies between them and that all parties are working on the same assumptions. Intended to prevent manipulation of data amongst other things, reconciliation disputes have led to vicious legal battles and massive company resources expended on a seemingly simple task. By implementing blockchain, firms can radically reduce the chance of reconciliation headaches by ensuring that the data all parties work with comes from a single immutable source. The governments of Italy and Dubai have experienced success working with this model, the latter of whom having already reduced reconciliation time by up to 45 days.

The success of bitcoin and other cryptocurrencies seems to be a less likely and more unpredictable trend for the moment. Little has happened since 2018 to suggest that cryptocurrencies will emerge as a genuinely major rival to traditional fiat ones, despite bitcoin’s recent price rise. More likely than the rise of bitcoin is that of central bank digital currencies. These would run on blockchain and are already being actively investigated by countries such as the UK and China, though their status and likelihood of being implemented remains uncertain.

The energy sector is one where blockchain has had less of an impact but still wields massive potential. Here, its primary influence will be to facilitate peer-to-peer (P2P) renewable energy trading. Presently, installing infrastructure to generate renewable energy is generally considered a poor investment for the everyday consumer, given the large capital costs and difficulties of selling excess energy one’s household does not use. Blockchain, through its ability to facilitate small-scale transactions between actors who do not trust one another, can address the latter of these issues. It does this through P2P trading, which essentially allows anyone within a certain area (known as a microgrid) to directly trade renewable energy they have produced with other participants. Multiple pilots trialling such systems are already in existence, with the Brooklyn Microgrid and Australian start-up Power Ledger prominent examples that have enjoyed local successes. Indeed, a recent report by the latter of these organisations revealed that through blockchain P2P trading, the time it takes for a 15-kWh battery to pay for itself could be almost cut in half from around 16 years down to around eight and a half. Though blockchain isn’t necessarily the only way to conduct P2P trading, it is currently the best one available. The extent of success firms such as Power Ledger achieve could therefore act as a major catalyst in accelerating the transition from central to distributed energy resources.

A notable aspect of blockchain that makes it less obvious as an innovation is that many of the positive changes it has inspired are away from the Western public eye, either in industries that receive little publicity or foreign countries. For instance, the shipping industry has already capitalised on blockchain and pushed its development further. Here, multiple consortiums such as IBM and Maersk’s TradeLens have placed blockchain at the centre of logistical planning. Asian countries have meanwhile harnessed blockchain’s power at a generally quicker rate than Western ones. In South Korea, government has been quick to adopt the technology, with the port city of Busan even earning the designation “regulation-free blockchain zone” after President Moon Jae-In described the progress of blockchain as a “matter of survival”.

Despite its massive potential, there are valid criticisms still to be made of blockchain. Despite its proponents’ claims to promote clean energy and saving on transaction costs, mining uses an immense amount of energy, slows down processes and results in transaction fees. Indeed, a University of Cambridge estimate claimed that bitcoin mining uses 0.2% of global energy supply, more than the entirety of Switzerland. Furthermore, bitcoin can only process an average of 4.6 transactions/second, compared to Visa’s 1,700 while also charging a fee of a few dollars per transaction. Security concerns over the technology also linger. The notorious 51% hack, for instance, where an actor gains control of over 50% of the mining power and can reverse transactions, remains elusive to solve. Indeed, just earlier this year Ethereum Classic, which is one of the very largest players in blockchain, saw $5 million drained from it by 51% hackers. Solutions are being promoted to address these issues, with the rise of Proof-of-Stake mining and sharding significantly helping to address inefficiencies and power concerns. However, the development of such processes is far from complete, and structural changes to enhance the security and operation of blockchain technology need to be made before it can reach its full potential.

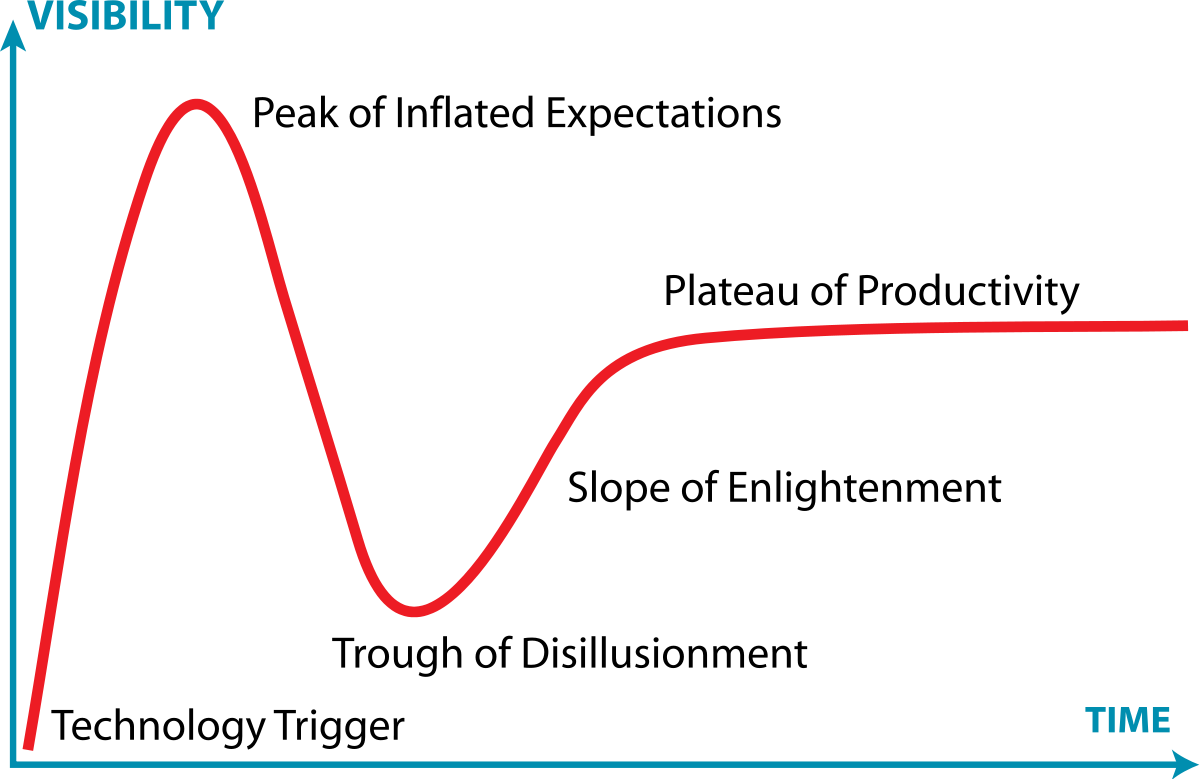

Ultimately, blockchain will go down as another victim of the Gartner Hype Cycle. This dictates that new innovations tend to result in an initial flurry of mass excitement before disappointment that the technology is not fully ready to use emerges. Then comes our current stage with blockchain, the slope of enlightenment, where people tone down their expectations and learn how the technology may be productive in a possibly more limited way than first expected. As the dot-com bubble demonstrated, any phenomenom can fall foul to this cycle. However, unlike the internet, blockchain’s impact on the world will be and has been far more subtle. While the replacement of cash with crypto seems to still be a long way off, blockchain has had a major impact on certain processes within the shipping and financial industries amongst numerous others. Most of the changes it has inspired, however, are not obvious ones that will “wow” the everyday consumer. Instead, they are working behind the scenes to slowly transform how processes within industry work, resulting in greater efficiency and security.

The views expressed in this article are the author’s own, and may not reflect the opinions of The St Andrews Economist