By Cameron Fulton

Originally coined in comedic condemnation of fiscal policy post-Great Depression, the term ‘trickle-down’ economics has stuck for almost a century. Coined by vaudevillian Will Rogers to lament Herbert Hoover in 1932, the quip has morphed into a theory in itself:

“The money was all appropriated for the top in the hopes that it would trickle down to the needy. Mr. Hoover was an engineer. He knew that water trickles down. Put it uphill and let it go and it will reach the driest little spot.”[i]

At the time of writing, unemployment had reached 22.5%. Mr Hoover had enforced a reduction in higher-income taxation and “saved the big banks, but the little ones went up the flue”[ii]. Hoover thought if the prosperous gained further wealth, they would expend it, meaning prosperity would ‘trickle-down’ into the lower echelons of social class. And whilst there would be a loss of tax revenue, this would be repaid by economic growth and prosperity over-time.

“But he didn’t know that money trickled up”[iii].

President Hoover ultimately could not survive the economic catastrophe of his tenure, leading to Democratic dominance over the next two decades. Inequality widened and debt rose by $6 billion during his tenure, and he is now widely considered one of the worst Presidents in US history.

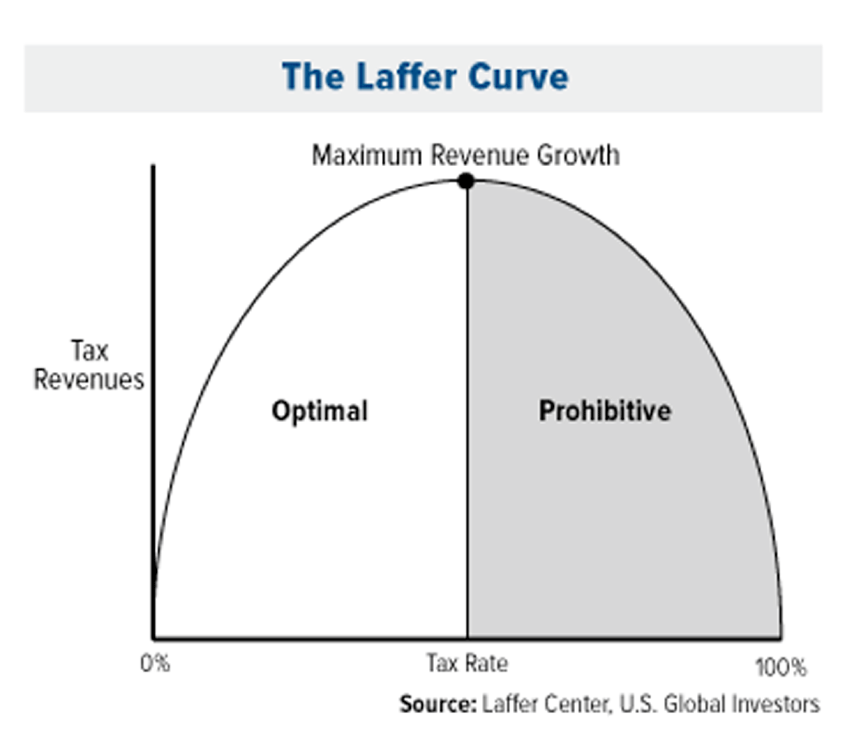

Fast-forward four decades to 1974, when economist Art Laffer met with Republican minnows, Dick Cheney and Donald Rumsfeld, and drew a curve on a napkin. A seemingly meaningless beer-after-work with a sprinkle of doodling has now become a famous anecdote, defining a tenet of Republican domestic economic policy in the coming forty plus years. That curve, now titled after its artist, professionalised Mr Rogers’ phrase.

The Laffer curve, seen above, observed a relationship between tax rate and subsequent revenue. Its inverse parabola proposed a tax rate associated with an optimal taxation revenue. Laffer believed taxation rates to be too high – a reduction would cause private sector growth that could fill lost revenue with economic prosperity, and subsequent streams of taxation.

A decade later, these men were no longer small fish. Laffer’s ideology became a core principle of Reagan-economic policy, or the now-famous ‘Reaganomics’, defined in a 1981 interview with David A. Stockman. The synonymous supply-side policy allowed for economic growth by reducing the progressive tax system, with freed-up markets putting employment in the hands of the private sector.

Reaganomics saw an escape from stagflation, reasonable economic growth and ultimately recovery from the 1980 economic crisis. The US was on the up and discussions of ideology was put to bed: capitalism had beaten communism, a policy goal since the second world war, that had been never convincingly settled. On paper, Laffer-infused Reaganomics was working.

But the trickle-down theory was a trickle-up policy once more.

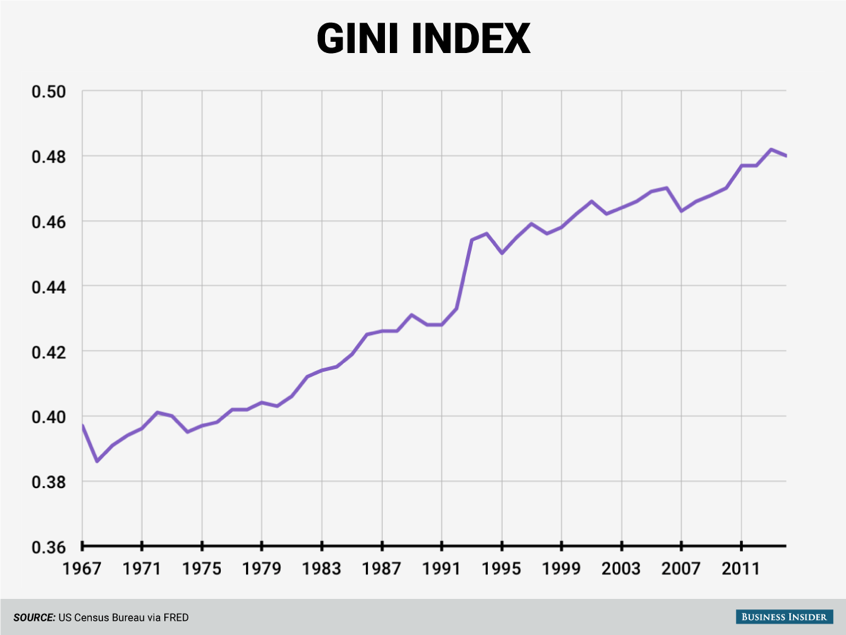

Inequality grew into a flagrant failure of government policy. The tax relief expected to distribute wealth across the population instead was retained by higher income individuals and corporations. The free market left behind the lower classes as money only trickled upwards. Between 1979 and 2005, there was only 6% growth in after-tax household income for the bottom fifth. For the top fifth, it was 80% growth. The Gini-coefficient, the most recognised measurement of inequality, rose steadily from under 0.4 in 1971 to over 0.46 post-millennium as shown below. Whilst the richer were getting richer, the poor were getting proportionately poorer.

Bush Jr used a similar policy in 2001 to end that year’s recession, with the Economic Growth and Tax Relief Reconciliation Act (EGTRRA). The results were the same as before: respectable short-term growth, but worsened income distribution and a higher budget deficit. Failing to repeal the EGTRRA, once the economy had been bolstered into a healthy state led to a housing market bubble and subsequent financial crisis in 2008.

Academics have been incensed by the notion for decades. Economist Joseph Stiglitz condemned trickle-down theory for years, debunking the proclaimed effects on the US economy, and ultimately concluded ‘a great divide’ was being created[iv]. He believed tax relief would be better given to lesser-income households; whose limited disposable income would far likelier be spent rather than saved. Thomas Piketty is another, who in his bestseller ‘Capital’ proved, empirically, tax cuts on the rich do not incentivise greater economic growth.

But in 2013, Kansas state governor Sam Brownback went against such critics as he attempted to implement extreme top-income tax reductions. Top individual state income-tax rate fell from 6.45% to 4.9% and non-wage income tax on smaller businesses was eliminated. It was advised that such reductions would be paid by economic growth and further employment.

Instead the state saw $338 million less-than-expected taxation revenue for 2014; a reduced state credit-rating; fiscal spending in tatters with forced spending cuts to education and social services; and job creation ranked 45th amongst US states for 2015. Brownback moved on from the post in 2018. Republican governance of the state moved on in 2019. Yet the theory remains part of domestic US policy.

A key fiscal goal of the Trump 2016 campaign, mass tax reductions on corporations were expected to encourage US GDP. The policy was propelled by who else but Mr Laffer, decreeing “if you cut that tax rate to 15%, it will pay for itself many times over… this will bring in probably $1.5T net by itself”. Mitch McConnell was another who suggested tax cuts “pay for themselves”.

And the rhetoric struck gold at the polls. The findings of the academics and the Kansas experiment were ignored. A $1.5 trillion tax-cut package was implemented in 2017, and the results were akin to historical consequences.

Trump’s Reagan-like policy saw GDP growth move to 3% for 2018 and maintained an upward trajectory pre-COVID. Employment reached an 18-year high. Polls were down but competitive, and ultimately re-election did not seem improbable, pre-COVID.

But in reality, such policies, as years gone past, have led to weakening fiscal indicators that ultimately harm longer-term growth. Tax revenue has failed to reap the rewards proposed by Republican frontmen, with a $183 billion loss when compared to projections in 2018. Little has been done in amending income distribution, with the top 20% of the population holding 52% of US income and the Gini-coefficient still following an upward trajectory. In search of re-election, economic policy has targeted news headlines rather than making real improvement in the long-term development of an ageing economic giant.

Trump, just last year, awarded Art Laffer the Presidential Medal of Freedom. And whilst, in theory, his neo-conservative policies would expect improvement to welfare and economic growth, empirically it is only the latter that receives a short-term gain. Indeed, he has become more a cable-news preacher, a CNN hullabaloo, than an economist – being declared the “world’s worst economist” by some.

COVID has thrown the US economy, along with the world, off course, and will dominate discussion in the lead-up to the November election – as it should. An inevitable collapse of economic growth, and catapulting unemployment rates have dominated the 2020 headlines.

Pre-COVID stats will likely be lauded as an indication of actual economic policy by the Republicans and will be seen as respectable at first glance. But behind this smokescreen is ultimately an economy that has regressed into a fragile social state.

The views expressed in this article are the author’s own, and may not reflect the opinions of The St Andrews Economist.

[i] ‘And Here’s How It All Happened’, Will Rogers, No. 518, St. Petersburg Times, November 27, 1932

[ii] ‘And Here’s How It All Happened’, Will Rogers, No. 518, St. Petersburg Times, November 27, 1932

[iii] ‘And Here’s How It All Happened’, Will Rogers, No. 518, St. Petersburg Times, November 27, 1932

[iv] ‘The Great Divide’, Joseph Stiglitz, April 20, 2015