By Matthew Fry

When Jerome Powell speaks, most people tend to listen. His task as head of the US Federal Reserve Bank (Fed) is setting monetary policy for the largest economy in the world. Quite rightly, he is extremely particular in his words. On March 26th, 2020, after the worst stock market crash since 1928, Powell addressed the press and the world. His message: “We are not going to run out of ammunition.” His statement preceded the staggered unveiling of the Fed’s truly titanic rescue packages. Slashed interest rates, quantitative easing, asset and bond ‘purchases’—the eye-watering magnitude of these interventions cannot be understated.

Since then, US and other central banks have seen the value of global assets under their control swell to over $20 trillion. The Fed alone now holds over $7 trillion of assets with the latest stimulus package announced this week. Amidst the crashing markets, plunging business activity, and devastating death tolls, the intrepid gaze of the market has fixated firmly on Powell. And one can be easily forgiven for misunderstanding his management of this most unsettling of economic shocks.

However, since the recent resurrection of global financial markets, speculators, analysts and journalists have been clambering over themselves to renounce the unholy Mr. Powell. Indeed, it has been levied that the Fed is no longer independent of government, and its programmes are massively expanding in size and control. There are concerns that by allowing the monumental amount of debt to burden the US taxpayer and economy, economic growth will slow for the foreseeable future.

They cite the black magic $7 trillion strong asset balance sheet, quantitative easing to finance US treasury for the new Coronavirus Aid, Relief, and Economic Security (CARES) Act, and the pinnacle of his market necromancy: the asset and bond ‘purchasing’ plans. However, Powell, has acted in the opposite way to the criticism - rescuing the US juggernaut whilst remaining a stickler for the rules.

However, the naysayers are only somewhat correct about the Fed’s balance. It is true that the total current assets in the Fed’s books are the highest they have ever been. But the danger of this has been vastly overstated.

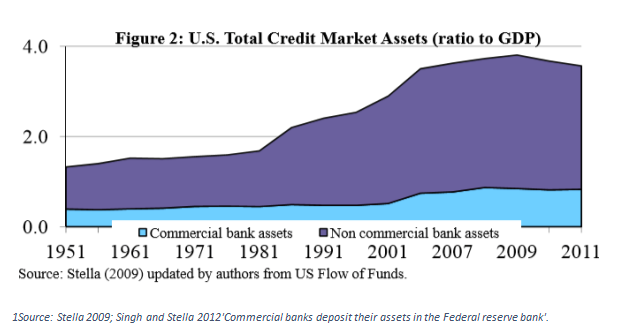

It is far safer for the Fed to hold private assets than before. Whilst in 2008, £1 in assets would have had £3 of other products reliant on it, now that figure will be closer to £2 of further reliant products— which vastly lowers the risk when scaled to trillions of dollars.

And Powell’s balance sheet ‘spending spree?’ Although the leviathan figure is the largest value ever recorded on the balance sheet, compared to the assets in the rest of the market, the Fed holds far less in assets than it has for most of its history. In fact, the ratio of assets held by the Fed compared to the assets in the hands of the private sector is far smaller than it has been previously. The light blue section in the graph below represents the ratio assets available to the Fed, to those held by the open market.

And what is more, Powell has not bought any assets off the open market and added them to the Fed’s balance sheet. How did the Fed accumulate these vast assets to his balance sheet, provide liquidity and calm to the markets in one fell swoop? A simple yet ingenious method, that has many speculators pointing the ‘market manipulation’ finger.

To add the non-treasury assets, the Fed has altered a current facility they offer to commercial banks. In the Fed’s normal remit is the purchase of treasuries (US government bonds under quantitative easing). The Fed can hold or sell off these treasuries to financial markets via the commercial banks. The system works both ways, where commercial banks can exchange any treasuries they own with the Fed, overnight, for cash.

Powell has altered this same facility to provide liquidity to commercial banks and vis a vis, the financial markets. Ingeniously, the Fed will exchange non-treasury assets that the commercial banks hold (stocks, bonds, and other securitised assets) for treasuries. This mechanism gives banks liquidity by being able to offload the private assets whose prices were plummeting under corona, and trade them quickly at a fair market value for treasuries from the Fed. The commercial banks can hold or swap these treasuries that they have exchanged through the new facility for their non-treasury assets instantly with the Fed.

This process shortens the date of government debt in the hand of the private sector (a small win for tax payers), it limits the mass sale of assets by the banks which would cause prices to plummet further, and it increases market confidence— because who in their right mind wants to fight the Fed? The Fed has then added private sector assets to its balance sheet, without changing its balance sheet, because for each dollar of non-treasury assets added, a dollar of treasuries is given to the commercial banks. Again, with some illusion and sleight of hand, Powell has evaded the mantle of market manipulation.

The CARES act is the immense fiscal package rolled out by the US treasury. The plan involves bailout and wage packages for large corporate entities, charities and the famed stimulus cheques sent out for the first time in US economic history. Which of course was financed through Powell and his money printers. The total cost of the first of two parts unleashed by the CARES act: $1.76 trillion. Brrr indeed.

Introduction of the CARES act has caused incorrect speculator assertions that the Fed has and continues to make risky purchases which to prop up insolvent or badly managed companies.

The CARES act allows companies to apply to the treasury (US government) to reimburse part of loans taken out to pay staff wages or keep businesses running. This includes the ‘Main Street lending programme’. To receive this reimbursement, companies must apply to commercial banks or other depositary institutions using a normal business loans procedure. Whilst the CARES act might be bailing out poorly managed companies, the Fed has nothing to do with these loans other than providing the additional money to the government through quantitative easing.

The final charge aimed at Powell is the Fed facilitating the exchange of credit for AAA rated corporate debt. The Fed will provide money to large corporates in exchange for high grade bonds with a maturity of less than 4 years. However, there is a clear difference between the Fed ‘buying’ bonds and the credit facility. The Fed will provide credit to the company in exchange for bonds, but it is the intermediary, who arranges the transaction, that is liable. That is, if the corporation that exchanged the bonds defaults whilst the Fed holds the same bonds, it will be the company that arranged the exchange that will be liable for the value of the lost assets. Again, Powell has deftly negotiated the levied accusations.

Understandably many around the world were baffled by a seemingly artificial stock market rise. Assets on the Fed’s balance sheet have hit their largest total value, and a litany of unseen policies have blurred people’s perception of the Federal Reserve. Whilst many were convinced that Powell and the Fed overstepped their remit into the US economy, they have performed strongly within the laws. It is Fed action along with a roaring performance for some of the Index’s largest weighted tech behemoths, that have performed strongly throughout turbulent market conditions.

However, with all the eyes on Powell, the real villain is escaping the criticism it deserves—the US government. It has taken tremendous risk to ‘counterbalance’ the economic crisis, which was in part caused by their extreme intercession into civil liberties: their lockdown policies, their forcible closure of business and offices. The CARES Act debt burden is an increase of at least $3 trillion —a large component of which has been given to companies who are undeserving of help.

Government action has swelled the budget deficit, which will ramp up future taxes and hinder economic growth. It is the taxpayer who will be paying the cost off for the foreseeable future—with no real reduction in corona deaths.

Our current conflict between the authoritarian left wing and nationalist populism is often linked to government intervention after the 2008 housing crash. One can only imagine the implication of the most recent policies. Although we have yet to see the full extent of the repercussions, Jerome Powell has been exceptional. His strong words have buoyed market confidence and sentiment. He has stuck firmly within this remit to stop the US economy from spluttering over the corona cliff and thundering into the rocks below.

The views expressed in this article are of the authors and may not reflect the opinions of The St Andrews Economist.