By Gary Mullins

Correspondent, Economics Undergraduate

Fed policy, equity sell-off and the return of volatility

It was another turbulent week in the global equity markets. The S&P 500 slid more than 5 per cent over the course of Wednesday and Thursday. The sell-off — sparked by investor fears over rising interest rates — was broad and painful, with every major US stock market index slipping below the 200-day moving average, a widely used measure of momentum. The sell-off may have started in the US but has rippled through Europe, Asia and emerging markets as the week progressed.

Strong US economic data released last week further compounded the Fed’s hawkish outlook on monetary policy. Investors are now taking into account the increased likelihood of higher interest rates when valuing equities. Higher rates increase the cost of debt thus deterring business investment. Reduced investment permeates through the economy, reducing production output and ultimately dampening investor outlook on corporate profits. Share prices fall accordingly.

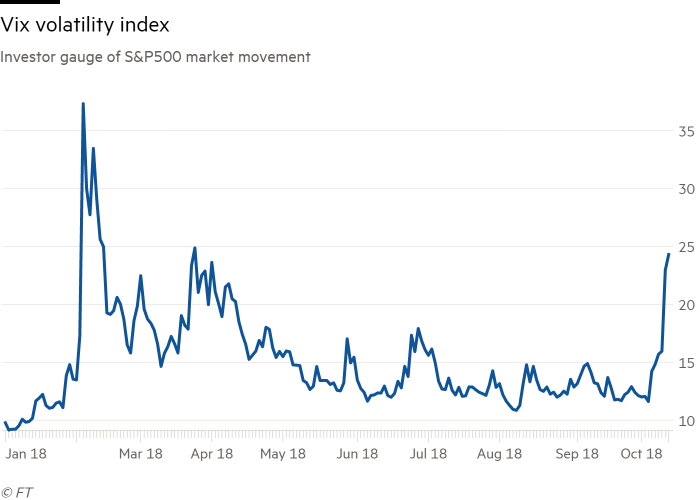

A direct implication of this week’s equity rout is the volatility spike it caused. The Cboe Global Markets Vix index of implied equity volatility— investors’ so-called “fear gauge” — peaked at 28.6, the highest since February, and well above its long-term average of 20. The Vix index is a widely used measure of market risk. In February of this year, the metric surged amid severe ructions in the volatility strategies used by algorithmic trading firms. Many see the Vix index as being intrinsically and dangerously flawed. When algorithmic funds see an uptick in volatility, they automatically unwind their risky positions in an attempt to reduce their exposure. However, the sell-off reduces equity prices - putting more volatility into the market and the Vix index continues to rise in a self-fulfilling manner. Under pure algorithmic trading, this process will continue ad infinitum.

Equities

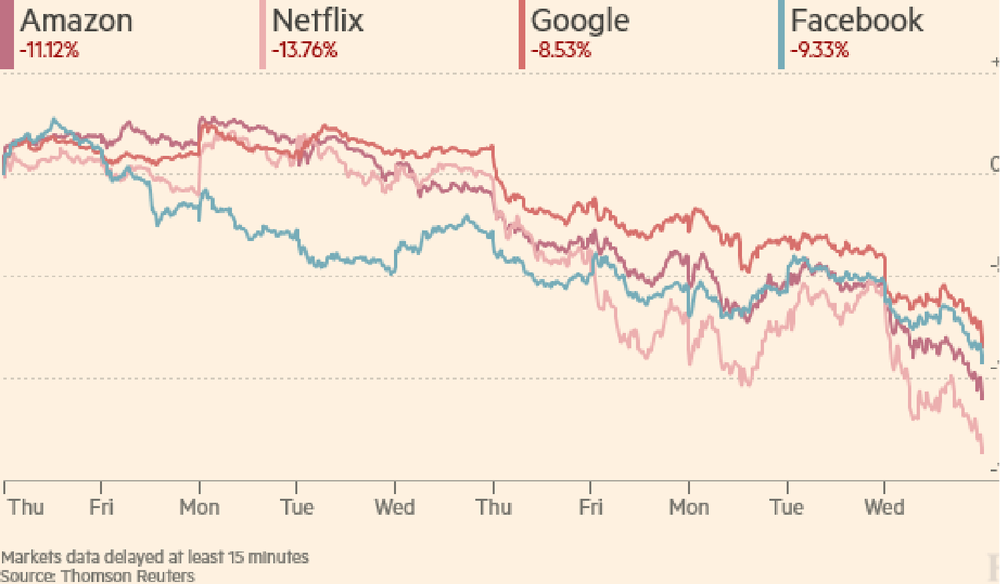

This week’s equity pullback left the S&P 500 more than 7 per cent below its recent record high, despite re-gaining some ground on Friday. Wednesday saw the heaviest losses with the S&P 500 suffering its biggest one-day retreat since February 8. The Dow Jones Industrial Average ended 3.2 per cent lower while the tech-heavy Nasdaq Composite shed 4 per cent, leaving it just a hair’s breadth away from correction territory. A correction is defined as a 10 per cent drop from the current economic cycle peak. Many investors are worried that traditionally lucrative technology stocks have become irrationally overpriced. The biggest technology firms are valued at many multiples of their underlying intrinsic value. Stronger global headwinds could result in a correction, particularly against the backdrop of data privacy concerns and the ongoing debate between freedom of speech and censorship on social media platforms.

Across the Atlantic, the pan-European Stoxx 600 index fell 2 per cent, with the Xetra Dax in Frankfurt ending 1.5 per cent and London’s FTSE 100 shedding 1.9 per cent. There were even steeper losses for Asian markets. The Shanghai Composite index fell 5.2 per cent, the Topix in Tokyo shed 3.5 per cent and the tech-heavy Taiwanese market tumbled 6.3 per cent.

Fixed- Income

Last week’s Treasury rout caused yields to surge by 17 basis points to 3.23 per cent. The pressure on yields continued this week when, on Tuesday, the 10-year US Treasury yield reached a seven-year peak of 3.261 per cent. Elsewhere, Monday’s trading saw Italian 10-year government bond yield jumped 16 basis points to end at 3.57 per cent. The sell-off of Italian bonds continued following last week’s announcement of a planned increased in government expenditure, despite already running the second largest deficit of any European nation. As investors offload Italian bonds, prices fall and, correspondingly, yields rise (bond yields and prices move in the opposite direction).

FOREX

Brexit consternation was reflected in the volatility of the sterling. Markets struggled to predict the impact of what appear to be ‘two steps forward, one step back’ Brexit negotiations. Sterling briefly reached a three-week high before ultimately remaining flat at $1.3159 to the dollar. The dollar found some support from rising Treasury yields. In Friday’s trading, the index tracking the currency against a basket of peers was up 0.3 per cent at 95.26c. Rising yields make US investment more attractive and increase capital inflows, resulting in upward pressure on the dollar. The euro managed to shrug off concerns about Italian fiscal policy, remaining flat for the week.

Commodities

Brent crude oil was down over 4 per cent this week, following last week’s four-year high of $86.74. Concerns stemmed from the potential impact of Hurricane Michael on oil production. On Wednesday, US oil producers evacuated platforms as a preventative measure against what was one of the most powerful storms in American history.

Gold ended the week up $28 at $1,217 an ounce. Historically, gold is seen as a safe haven - an investment that is expected to retain or increase in value during times of market turbulence. Investors turn to such assets to mitigate their exposure to market downturns.

The Week Ahead

Investor attention will be firmly focused on the EU leaders’ summit in Brussels this week with Brexit, migration and the Eurozone on the menu. There are hopes that a draft version of the EU-UK future relationship can be thrashed out despite the Irish backstop issue remaining a sticking point for both sides. Even though it appears that Ms May will return with a first stage agreement, the second stage - setting up the official EU-UK trade framework – will inevitably be more fractious.

Investors will also be watching Chinese expected economic growth data amid an increasingly frayed relationship between the world’s two largest economies. President Trump imposed punitive tariffs of $50b on Chinese imports in July and a further $200b in September. Chinese investment and economic growth is already slowing due to a government crackdown on risky lending practices and the devaluing of the Renminbi.

First photo provided by FT Market Data

Second photo provided by Thomas Reuters

References

FT Markets Overview:

https://www.ft.com/content/681af048-cdc3-11e8-9fe5-24ad351828ab

https://www.ft.com/content/c6151f3e-ccf1-11e8-9fe5-24ad351828ab

https://www.ft.com/content/fbf7cb36-cc30-11e8-9fe5-24ad351828ab

https://www.ft.com/content/b3e65360-cb65-11e8-b276-b9069bde0956

https://www.ft.com/content/6b5c4328-ca90-11e8-9fe5-24ad351828ab

Equity sell-off:

https://www.ft.com/content/a6292072-ce35-11e8-9fe5-24ad351828ab

Vix index:

https://www.ft.com/content/af34550e-cd01-11e8-b276-b9069bde0956

Last week’s rundown:

https://thestandrewseconomist.com/2018/10/08/the-market-this-week-8-october/

Dollar strength:

https://www.ft.com/content/8d4ac0c6-ce56-11e8-b276-b9069bde0956

The Week ahead:

https://www.ft.com/video/c87dc7b3-46e3-4c68-9644-12fa22ac4360